The Estate Tax “Cliff” Is Gone. So Why Are Oklahoma Attorneys Still Talking About Portability and Disclaimer Trusts?

ESTATE PLANNING

Charles M. Woner

7/17/20264 min read

For years, married couples heard the same warning: the federal estate tax exemption was scheduled to be cut roughly in half at the end of 2025. That sunset never arrived. The One Big Beautiful Bill Act made the higher exemption permanent, and for 2026 each person can transfer $15 million free of federal estate tax — $30 million for a married couple — with inflation adjustments going forward.

Here in Oklahoma, where we have no state estate tax, it’s tempting to conclude that estate tax planning is finished business for all but a handful of families. It isn’t. Two tools — portability and the disclaimer trust — remain the quiet workhorses of a well-built marital estate plan. Here’s why.

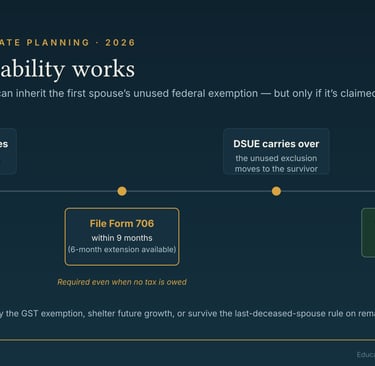

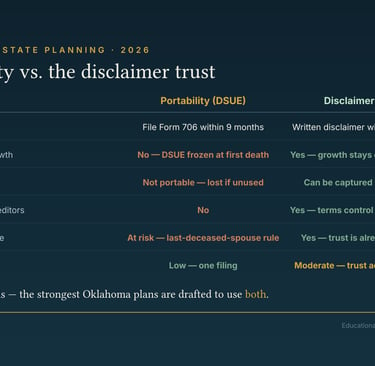

Portability: the exemption that follows the surviving spouse

When the first spouse dies, any portion of their $15 million exemption they didn’t use doesn’t have to be wasted. The unused amount — the Deceased Spousal Unused Exclusion, or “DSUE” — can be carried over to the surviving spouse.

But there’s a catch that trips up families every year: portability is not automatic. For most estates under the filing threshold, no federal estate tax return is due at all — which is exactly the trap. The only way to capture the DSUE is to file Form 706 voluntarily, generally within nine months of death (a six-month extension is available). Skip that filing, and the first spouse’s exemption is generally gone. The IRS does offer a simplified late-election procedure for estates not otherwise required to file, currently allowing up to five years, but relying on cleanup relief is never a plan.

Portability also has real limits:

• It doesn’t cover the GST exemption. The generation-skipping transfer tax exemption — critical for families planning for grandchildren — dies with the first spouse if it isn’t used.

• It doesn’t shelter growth. The DSUE is frozen at the first death. If the surviving spouse holds appreciating assets — and in Oklahoma that often means ranch land, mineral interests, or a family business — every dollar of growth lands in the survivor’s taxable estate.

• Remarriage can complicate it. Only the last deceased spouse’s unused exemption counts.

• It offers no asset protection and no control over where assets ultimately go — a real concern in blended families.

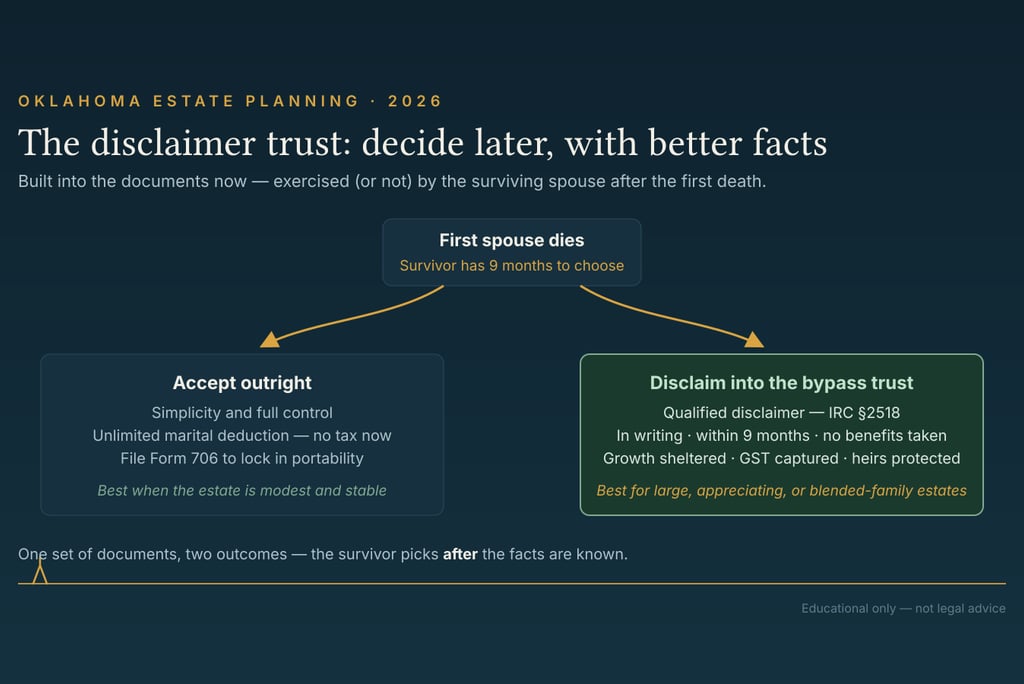

The disclaimer trust: flexibility you build in now, decide on later

A disclaimer trust flips the timing of the decision. Instead of locking in a complex trust structure today for a tax problem that may never materialize, the estate plan leaves everything to the surviving spouse outright — but gives the survivor the option to redirect some assets into a bypass (credit shelter) trust after the first death.

The mechanism is the qualified disclaimer under Internal Revenue Code §2518. Within nine months of the first spouse’s death, the survivor may formally decline — “disclaim” — some or all of the inheritance. To qualify, the disclaimer must be in writing, made within nine months, made before the survivor accepts any benefit from the disclaimed assets, and the assets must pass without the survivor’s direction. Disclaimed assets then flow into the trust the couple’s documents already created.

Why is that so useful?

• It’s a wait-and-see strategy. The survivor decides with full knowledge of the asset values, the tax law, and the family circumstances as they actually exist — not as they were guessed at years earlier.

• Growth inside the trust is sheltered. Assets disclaimed into the bypass trust, plus all their future appreciation, generally stay out of the survivor’s taxable estate.

• It can capture the GST exemption that portability would forfeit.

• It adds protection. Trust assets can be insulated from the survivor’s future creditors and preserved for the couple’s children — including children from a prior marriage.

The trade-off is discipline: the surviving spouse must act within nine months and cannot have touched the assets first. That’s exactly why these plans need to be drafted — and administered — with care.

Why the smart Oklahoma plan often uses both

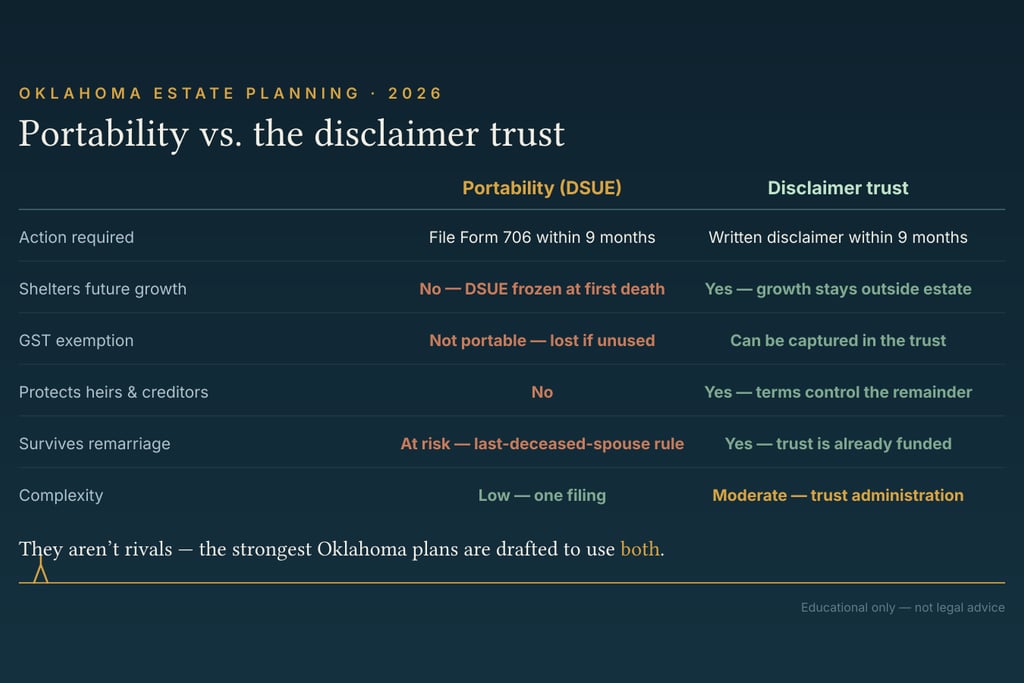

Portability and disclaimer trusts aren’t rivals. The most resilient marital plans layer them:

• Draft the disclaimer trust option into the documents now, while both spouses are living and healthy.

• At the first death, evaluate. If the combined estate is comfortably below the exemption and simplicity wins, the survivor takes outright and the executor files Form 706 to lock in portability as a backstop.

• If the estate is large, growing, or the family situation calls for protection, the survivor disclaims the right amount into the trust — capturing GST exemption, freezing appreciation outside the taxable estate, and protecting the remainder.

And the two tools can work in the same estate at the same time. Section 2518 permits partial disclaimers, so a surviving spouse might disclaim only the appreciating assets — the ranch, the minerals, the closely held business — into the bypass trust, then have the executor file Form 706 to port whatever exclusion remains unused. The result: sheltered growth and GST coverage inside the trust, plus a DSUE backstop stacked on the survivor’s own exemption.

“Permanent” tax law is only as permanent as the next Congress. A plan built with both tools works whether the exemption stays at $15 million, climbs with inflation, or gets cut in a future budget deal.

If your will or trust was drafted before 2026 — or if it was built around the old sunset that never happened — it’s worth a fresh look. Nine months goes by faster than any grieving family expects.

Charles M. Woner (OBA #33789) practices estate planning and probate law in Oklahoma. This article is for general informational purposes only and does not constitute legal or tax advice. Reading it does not create an attorney-client relationship. Consult a qualified attorney about your specific circumstances.

Contact

5300 N. Shartel Ave., #18622

Oklahoma City, OK 73118

Phone